Financial and Management Accounting for CFOs and Founders

One tells you what happened. The other tells you what to do next. Most companies treat them as the same function and pay for the confusion in slow decisions and missed opportunities.

Walk into almost any growing company and ask the founder what their accounting team does, and you’ll get a vague answer about “the books.” Ask the same question to a seasoned CFO, and you’ll get a much sharper one – because experienced finance leaders know that accounting isn’t a single discipline. It’s two. And the failure to distinguish between financial accounting and management accounting is one of the quietest, most expensive mistakes a leadership team can make.

This isn’t an academic distinction. It’s the difference between having books that satisfy your auditor and having a finance function that actually helps you run the business. For CFOs, controllers, CPA firm owners, and founders who want both, understanding how these two disciplines differ and where they overlap is foundational.

The Core Difference, in One Sentence

Financial accounting exists to tell people outside your company what has already happened. Management accounting exists to help people inside your company decide what to do next. Everything else — the GAAP requirements, the reporting cadence, the audit trails, the level of granularity — flows from that single distinction.

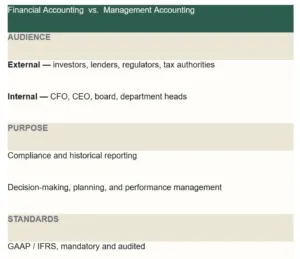

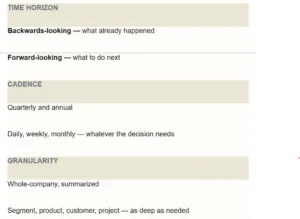

Financial accounting is governed by external standards. In the United States, that means GAAP, set by the Financial Accounting Standards Board, and for public companies, additional SEC oversight. The output is the familiar trio of statements: the income statement, the balance sheet, and the cash flow statement. These are produced on a fixed cadence — quarterly and annually — and they’re built to be comparable across companies, audited by independent firms, and trusted by investors, lenders, regulators, and tax authorities. Financial accounting is rigorous, standardized, and deliberately backwards-looking.

However, management accounting, by contrast, is built for the people sitting around your leadership table. There are no mandatory standards, no required formats, and no external audit. The output is whatever the business actually needs to make better decisions — a 13-week cash forecast, a contribution-margin analysis by product line, a customer profitability report, a budget variance dashboard, a break-even model for a new market. Management accounting is flexible, granular, and deliberately forward-looking.

Where Do Financial and Management Accounting Diverge, Side by Side

But Why Does the Distinction Between Financial and Management Accounting Matter?

Here’s where most articles on this topic stop. They lay out the differences and assume the reader will figure out the implications. The implications are the whole point.

When a leadership team confuses financial accounting with management accounting, they end up making operational decisions from GAAP financial statements. That’s a problem because GAAP statements are designed for comparability and compliance — not for clarity about which product line is actually profitable, which customer is silently destroying margin, or where the next ninety days of cash pressure are coming from. A P&L that complies with revenue recognition rules can completely obscure the unit economics that are quietly killing the business.

A clean income statement can tell you the company made money last quarter. It doesn’t tell you a single useful thing about whether you should keep doing what you’re doing.

The reverse mistake is just as costly. Companies that lean entirely on internal management reports without disciplined financial accounting end up with audit problems, lender covenant violations, and fundraising rounds that fall apart during due diligence. Investors don’t want your dashboard. They want clean, GAAP-compliant statements that they can trust. The two disciplines aren’t substitutes. They’re complements, and a high-performing finance function intentionally builds both.

Also, there’s a talent dimension worth naming. Financial accountants are trained to be precise, rule-bound, and cautious. These are the qualities you absolutely want when the auditor walks in. Management accountants (and the FP&A professionals who increasingly do this work) are trained to be analytical, hypothesis-driven, and comfortable with imperfect data. These are different skill sets, and asking one person to do both well is asking a lot. Smaller companies often have to, but as a finance function matures, separating the two responsibilities. Even if one person still owns both, it is usually a turning point in the quality of insight leadership receives.

How Do the Best Finance Teams Architect Both?

In a well-run finance function, financial accounting and management accounting share a single source of truth—the general ledger—but serve entirely different consumers. The financial accounting workflow flows toward compliance: monthly close, reconciliations, accruals, GAAP-compliant statements, audit support, and tax preparation. The management accounting workflow flows toward decision-making: KPI dashboards, FP&A models, rolling forecasts, variance analysis, scenario planning, and capital allocation reports. The same underlying transactions feed both, but the framing, the cadence, and the audience are fundamentally different.

What’s changed now is the technology layer connecting them. Modern finance platforms, combined with AI-driven anomaly detection, predictive cash flow modelling, and real-time consolidation, have narrowed the time gap between the two disciplines. The historical data that financial accounting captures can now feed forward-looking management reports in near real time. Earlier, it would arrive three weeks after the month-end, when the decisions had already been made. CFOs who build their function around this convergence get something the legacy model never delivered. They get compliance and insight from the same data, refreshed continuously.

The Take Away for Finance Leaders

The question isn’t which discipline matters more. Both matter, and both serve different masters. The question is whether your finance function is structured to deliver well on both. Clean GAAP-compliant statements for the outside world, and sharp, decision-grade reporting for the leadership team to act on what those numbers mean. For CFOs and founders willing to invest in intentionally building both sides, the payoff is a finance function that doesn’t just report the past. It should actively shape what comes next. That’s the real reason this distinction matters. Not because it shows up in textbooks. Because it shows up in the decisions that determine whether the business grows or stalls.